B2B payment processing: understanding methods, challenges, and solutions

B2B payment processing serves as the financial backbone of businesses, covering transactions like supplier payments and service invoices. Unlike consumer transactions, B2B payments are more intricate, involving larger sums, multi-layered approval processes, and stringent security measures. As businesses expand globally, streamlining and optimizing payment processes become essential to ensuring seamless financial operations. This article delves into the complexities of B2B payment processing, challenges faced by businesses, common payment methods, and strategies to select the best solutions.

What is b2b payment processing?

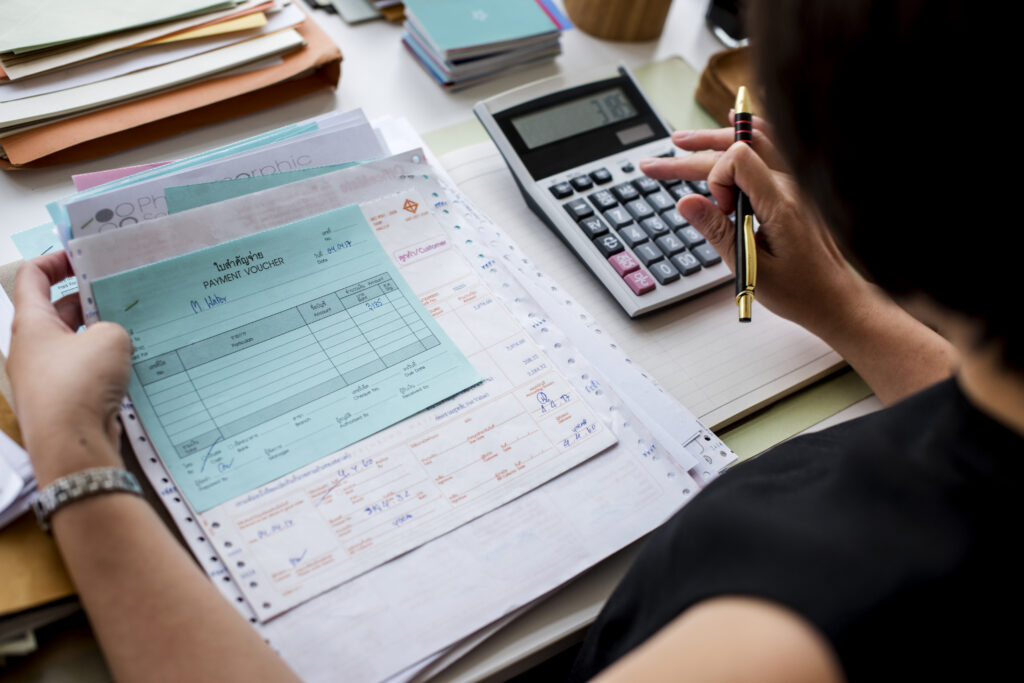

B2B payment processing refers to the systems and methods used to facilitate payments between businesses. Whether it’s a retailer paying a wholesaler or a corporation settling a service provider’s invoice, these transactions are vital to business continuity. Unlike B2C payments, which are often quick and straightforward, B2B transactions require customized invoicing, multiple layers of approval, and negotiated payment terms.

One of the primary distinctions of B2B payments is the high transaction value. Business payments often run into millions, compared to the smaller, more frequent payments typical in consumer markets. Another key difference is the payment cycle—B2B transactions typically follow longer timelines, ranging from 30 to 90 days, depending on agreements between the parties.

Additionally, businesses rely on a diverse range of payment methods, including ACH transfers, wire transfers, corporate credit cards, and even traditional checks. The choice of method depends on transaction size, industry standards, and specific agreements between the transacting businesses. Compliance and documentation also play a significant role in ensuring smooth transactions, requiring businesses to maintain detailed financial records and adhere to regulatory requirements.

Why b2b payment processing is essential

Efficient B2B payment processing offers multiple benefits that enhance a company’s financial health and operational efficiency.

Enhancing cash flow management

Timely payments are crucial for maintaining a healthy cash flow. Delays in payments can disrupt supply chains, strain relationships with vendors, and even result in financial penalties. Businesses that optimize their payment processes can ensure that suppliers and service providers are paid on time, leading to stronger partnerships and improved business efficiency.

Reducing manual errors and improving automation

Automation has revolutionized B2B payment processing, helping businesses minimize human errors, streamline workflows, and save valuable time. Automated invoicing and payment solutions reduce administrative burden, allowing finance teams to focus on strategic decision-making rather than routine transaction management.

Lowering transaction costs

Traditional B2B transactions, especially those involving paper-based processes, can be costly. Adopting digital payment solutions such as ACH transfers and electronic invoicing can significantly reduce transaction costs, making payments more cost-effective and efficient.

Strengthening security and fraud prevention

Given the high value of B2B transactions, security is a top priority. Businesses must implement robust security measures like encryption, multi-factor authentication, and fraud detection systems to safeguard sensitive financial information. Additionally, ensuring compliance with global financial regulations mitigates the risk of financial fraud and legal penalties.

Key challenges in b2b payment processing

Despite its advantages, B2B payment processing presents challenges that businesses must address to optimize their financial operations.

Managing complex approval processes

B2B payments typically involve multiple stakeholders, including procurement teams, finance departments, and external vendors. Each stakeholder has distinct requirements, leading to a complex approval process. For example, a procurement manager may need to authorize a purchase before the finance department processes the payment.

To overcome this challenge, businesses should implement automated approval systems that streamline communication and reduce delays. These systems ensure that all parties have real-time access to transaction statuses, enhancing transparency and efficiency.

Addressing high transaction values and security concerns

B2B transactions often involve substantial sums, making them attractive targets for cybercriminals. Payment fraud, data breaches, and unauthorized transactions are common threats that businesses must guard against.

Implementing strict security measures—such as tokenization, real-time fraud monitoring, and secure payment gateways—can help mitigate risks. Additionally, employee training on fraud prevention and regulatory compliance enhances security awareness across the organization.

Ensuring compliance with financial regulations

B2B payment processing must comply with various regulations, such as the Payment Card Industry Data Security Standard (PCI DSS) and the General Data Protection Regulation (GDPR). Non-compliance can result in hefty fines and reputational damage.

Businesses should adopt payment solutions that offer seamless integration with existing accounting and ERP software while ensuring compliance with global financial regulations. These solutions facilitate efficient tax calculations, automated reporting, and data security compliance, reducing the administrative burden on finance teams.

Choosing the right B2B payment solution

Selecting the right payment solution is critical for business efficiency and growth. Companies should consider several factors when evaluating payment processing solutions.

Compatibility with business needs

The ideal payment solution should align with a company’s operational requirements, industry standards, and transaction volume. Businesses should assess whether a solution supports preferred payment methods, integrates with existing software, and offers scalability as the company grows.

Cost-effectiveness and efficiency

Payment processing fees vary based on the solution provider and transaction method. Businesses should analyze transaction costs and evaluate cost-saving options, such as bulk payment processing, automated invoicing, and discounts for early payments.

Security and fraud protection features

Security should be a top priority when selecting a payment processor. Businesses should opt for solutions that offer advanced security measures, including encryption, fraud detection algorithms, and real-time transaction monitoring.

Customer support and reliability

A reliable payment processing partner should provide excellent customer support, ensuring that any issues or technical glitches are promptly addressed. Evaluating customer reviews and service level agreements can help businesses make informed decisions.

Common B2B payment methods

Businesses today have access to a variety of payment methods, each offering unique benefits and challenges. Selecting the right option depends on factors such as transaction size, security, speed, and cost-effectiveness. Understanding these choices can help businesses streamline their financial operations and maintain smooth transactions with suppliers, partners, and service providers.

Credit cards for convenience and flexibility

Credit cards remain a widely used payment method in the B2B sector, valued for their convenience and widespread acceptance. They are particularly useful for smaller transactions and immediate payments. Many businesses prefer credit cards due to their ability to track expenses easily and earn rewards, such as cashback and travel points.

However, using credit cards for large-scale payments can be costly due to high processing fees. Additionally, credit limits can impose restrictions on businesses looking to make significant purchases. Companies should also be cautious about interest charges, as carrying a balance can lead to increased financial burdens over time. Despite these downsides, credit cards offer a flexible and practical solution for managing cash flow in day-to-day business operations.

Bank and wire transfers for secure transactions

Bank and wire transfers are one of the most reliable methods for handling large transactions, both domestically and internationally. They provide security and traceability, making them ideal for businesses prioritizing financial accuracy and protection against fraud.

For international payments, wire transfers are particularly beneficial as they allow businesses to transfer large sums across borders. However, the costs can be substantial due to transaction fees and currency exchange markups. Additionally, wire transfers may take a few days to process, which can be a drawback for businesses requiring immediate funds.

Despite these challenges, many organizations continue to use wire transfers, especially when dealing with high-value transactions that demand a secure and verified process. To optimize costs, businesses can explore alternatives such as bulk transfers or partnerships with financial institutions offering lower fees.

ACH payments for recurring transactions

Automated Clearing House (ACH) payments are an efficient and cost-effective option for businesses that require frequent transactions. These payments are commonly used for payroll, subscription services, and supplier payments, allowing for seamless fund transfers between bank accounts.

ACH payments tend to be more affordable than wire transfers and are processed within a few days. While they are not ideal for urgent transactions due to processing delays, they offer a streamlined approach for companies managing recurring payments. The automation of ACH transactions also reduces human errors and administrative workload, making them a preferred choice for businesses looking to enhance efficiency.

Digital payment platforms and wallets

The rise of digital payment solutions has transformed the B2B landscape, making transactions faster, more efficient, and more accessible. Platforms such as PayPal, Stripe, and Square offer businesses the ability to send and receive payments with ease. These platforms often include additional features such as invoicing, real-time tracking, and fraud protection.

Digital wallets like Apple Pay and Google Wallet further enhance the convenience of mobile transactions. While these options provide flexibility, they may come with higher fees compared to traditional methods. Businesses must also ensure they have the necessary cybersecurity measures in place to protect sensitive financial information.

As digital payments continue to gain traction, more businesses are adopting these solutions to reduce reliance on traditional banking systems and improve payment efficiency.

The decline of cheques and cash payments

Despite technological advancements, some businesses still rely on cheques and cash for transactions. Cheques offer a tangible record of payments but are often slow to process, prone to errors, and susceptible to fraud. Additionally, cheque payments can take days or weeks to clear, causing cash flow delays.

Cash payments are even less common in B2B transactions due to security risks and challenges in tracking large amounts. As digital and automated payment methods become more widely accepted, businesses are gradually shifting away from cheques and cash to improve efficiency and security.

Trends shaping the future of B2B payments

The B2B payment landscape is constantly evolving, driven by technological advancements and changing business needs. Several key trends are influencing how companies handle financial transactions, making payments faster, more secure, and cost-effective.

The rise of automation in payment processing

Automation is revolutionizing B2B payments by reducing manual tasks and increasing accuracy. Automated invoicing, payment scheduling, and reconciliation help businesses avoid delays and errors. Software solutions like QuickBooks, Xero, and SAP streamline financial operations, ensuring timely payments and improved cash flow management.

By adopting automation, companies can allocate more resources to strategic planning rather than spending time on administrative tasks. Automation also helps prevent issues such as duplicate payments, miscalculations, and missed deadlines, further improving financial efficiency.

The shift towards digital and contactless payments

Businesses are increasingly adopting digital payment methods to enhance speed and security. Mobile payments, contactless transactions, and electronic fund transfers are gaining popularity, particularly as remote work and global trade continue to expand.

Blockchain technology and cryptocurrencies are also making inroads into B2B transactions. These technologies promise faster cross-border transactions, reduced costs, and enhanced security. While not yet mainstream, businesses dealing with international clients are exploring the potential of blockchain to simplify payment processes.

Enhanced security measures for fraud prevention

With the rise in digital transactions, cybersecurity has become a top priority for businesses. Companies are investing in advanced fraud detection systems, encryption technologies, and multi-factor authentication to safeguard financial transactions.

Regulatory bodies are also implementing stricter compliance requirements to ensure payment security. Businesses must stay updated with industry standards and invest in secure payment gateways to protect against fraud and cyber threats.

Common B2B payment methods

Businesses today have access to a variety of payment methods, each offering unique benefits and challenges. Selecting the right option depends on factors such as transaction size, security, speed, and cost-effectiveness. Understanding these choices can help businesses streamline their financial operations and maintain smooth transactions with suppliers, partners, and service providers.

Credit cards for convenience and flexibility

Credit cards remain a widely used payment method in the B2B sector, valued for their convenience and widespread acceptance. They are particularly useful for smaller transactions and immediate payments. Many businesses prefer credit cards due to their ability to track expenses easily and earn rewards, such as cashback and travel points.

However, using credit cards for large-scale payments can be costly due to high processing fees. Additionally, credit limits can impose restrictions on businesses looking to make significant purchases. Companies should also be cautious about interest charges, as carrying a balance can lead to increased financial burdens over time. Despite these downsides, credit cards offer a flexible and practical solution for managing cash flow in day-to-day business operations.

Bank and wire transfers for secure transactions

Bank and wire transfers are one of the most reliable methods for handling large transactions, both domestically and internationally. They provide security and traceability, making them ideal for businesses prioritizing financial accuracy and protection against fraud.

For international payments, wire transfers are particularly beneficial as they allow businesses to transfer large sums across borders. However, the costs can be substantial due to transaction fees and currency exchange markups. Additionally, wire transfers may take a few days to process, which can be a drawback for businesses requiring immediate funds.

Despite these challenges, many organizations continue to use wire transfers, especially when dealing with high-value transactions that demand a secure and verified process. To optimize costs, businesses can explore alternatives such as bulk transfers or partnerships with financial institutions offering lower fees.

ACH payments for recurring transactions

Automated Clearing House (ACH) payments are an efficient and cost-effective option for businesses that require frequent transactions. These payments are commonly used for payroll, subscription services, and supplier payments, allowing for seamless fund transfers between bank accounts.

ACH payments tend to be more affordable than wire transfers and are processed within a few days. While they are not ideal for urgent transactions due to processing delays, they offer a streamlined approach for companies managing recurring payments. The automation of ACH transactions also reduces human errors and administrative workload, making them a preferred choice for businesses looking to enhance efficiency.

Digital payment platforms and wallets

The rise of digital payment solutions has transformed the B2B landscape, making transactions faster, more efficient, and more accessible. Platforms such as PayPal, Stripe, and Square offer businesses the ability to send and receive payments with ease. These platforms often include additional features such as invoicing, real-time tracking, and fraud protection.

Digital wallets like Apple Pay and Google Wallet further enhance the convenience of mobile transactions. While these options provide flexibility, they may come with higher fees compared to traditional methods. Businesses must also ensure they have the necessary cybersecurity measures in place to protect sensitive financial information.

As digital payments continue to gain traction, more businesses are adopting these solutions to reduce reliance on traditional banking systems and improve payment efficiency.

The decline of cheques and cash payments

Despite technological advancements, some businesses still rely on cheques and cash for transactions. Cheques offer a tangible record of payments but are often slow to process, prone to errors, and susceptible to fraud. Additionally, cheque payments can take days or weeks to clear, causing cash flow delays.

Cash payments are even less common in B2B transactions due to security risks and challenges in tracking large amounts. As digital and automated payment methods become more widely accepted, businesses are gradually shifting away from cheques and cash to improve efficiency and security.

Trends shaping the future of B2B payments

The B2B payment landscape is constantly evolving, driven by technological advancements and changing business needs. Several key trends are influencing how companies handle financial transactions, making payments faster, more secure, and cost-effective.

The rise of automation in payment processing

Automation is revolutionizing B2B payments by reducing manual tasks and increasing accuracy. Automated invoicing, payment scheduling, and reconciliation help businesses avoid delays and errors. Software solutions like QuickBooks, Xero, and SAP streamline financial operations, ensuring timely payments and improved cash flow management.

By adopting automation, companies can allocate more resources to strategic planning rather than spending time on administrative tasks. Automation also helps prevent issues such as duplicate payments, miscalculations, and missed deadlines, further improving financial efficiency.

The shift towards digital and contactless payments

Businesses are increasingly adopting digital payment methods to enhance speed and security. Mobile payments, contactless transactions, and electronic fund transfers are gaining popularity, particularly as remote work and global trade continue to expand.

Blockchain technology and cryptocurrencies are also making inroads into B2B transactions. These technologies promise faster cross-border transactions, reduced costs, and enhanced security. While not yet mainstream, businesses dealing with international clients are exploring the potential of blockchain to simplify payment processes.

Enhanced security measures for fraud prevention

With the rise in digital transactions, cybersecurity has become a top priority for businesses. Companies are investing in advanced fraud detection systems, encryption technologies, and multi-factor authentication to safeguard financial transactions.

Regulatory bodies are also implementing stricter compliance requirements to ensure payment security. Businesses must stay updated with industry standards and invest in secure payment gateways to protect against fraud and cyber threats.

FAQs

What are the payment terms for b2b?

B2B payment terms often vary depending on the agreement between businesses. Standard terms include Net 30, Net 60, or Net 90, which refer to the days the buyer has to pay after receiving the invoice. Businesses may also offer discounts for early payments or require partial payment upfront.

What is the b2b billing process?

The B2B billing process typically involves generating an invoice that details the products or services provided, the payment amount, and the due date. The invoice is then sent to the buyer for approval, and once approved, the payment is processed. The process may include multiple steps, such as negotiating payment terms, sending reminders, and managing payment reconciliations.

What is the difference between b2b and b2c payments?

B2B payments are transactions between two businesses and usually involve more significant sums, longer payment cycles, and more complex approval processes. In contrast, B2C payments are between a company and an individual consumer, often involving more straightforward transactions and faster payment methods, like credit cards or digital wallets.

Is MasterCard b2b or b2c?

Mastercard operates in both B2B and B2C sectors. While it is well known for consumer credit and debit card services, it also offers solutions tailored for businesses, such as corporate and procurement cards, which facilitate B2B transactions.

Is b2b cheaper than b2c?

B2B transactions can be more cost-effective per transaction than B2C transactions, especially when using automated bank transfers like ACH. However, this depends on the payment method and its associated fees. Credit card fees, for instance, can be higher for B2B transactions, but overall costs can be reduced through efficient processes and negotiated terms.